MARKET OVERVIEW

Transactions involving well-priced, well-placed commercial property trickled in during the quarter. Industrial deal activity hovered close to its historical average. Prospects for retail properties were boosted by continued consumer spending at restaurants and retail openings (particularly by discount stores) which outpaced store closings. The CRE markets remained weighed down by inhospitable financial conditions. In addition to more interest rate rises, lenders tightened standards in the wake of banking troubles and the good standing of U.S. debt was in question. According to Trepp®, the commercial mortgage-backed securities (CMBS) market also atrophied. Cap rates inched up for all property types and transaction volume dropped by 59 percent over the first four months of the year, per MSCI. But some of this fall-off was attributable to reduced prices (the RCA CPPI National All-Property Index was down over nine percent from last year) as the market adjusted to its new reality. In terms of the number of properties, sales shrank 24 percent in the first quarter.

The Apartment sector, where transaction volume noticeably faltered, was in the spotlight – but long-term worries were muted. As RCA Capital Trends noted, “In truth, the market simply slipped back closer to a normal level this year.” Demand for apartments is almost assured, due to elevated levels of household formation and the persistent single-family home affordability issue.

Office was the one area showing true signs of stress entering Q2 2023. Per JLL, the vacancy rate breached the 20 percent mark and the Mortgage Bankers Association showed delinquencies increasing by 110 basis points.

By the end of July, there may be a lessening of the broad unease in the markets. The Fed has indicated that it may increase rates again in June, the debt ceiling impasse is being resolved and dramatic revelations about regional banks could be in the rear-view mirror.

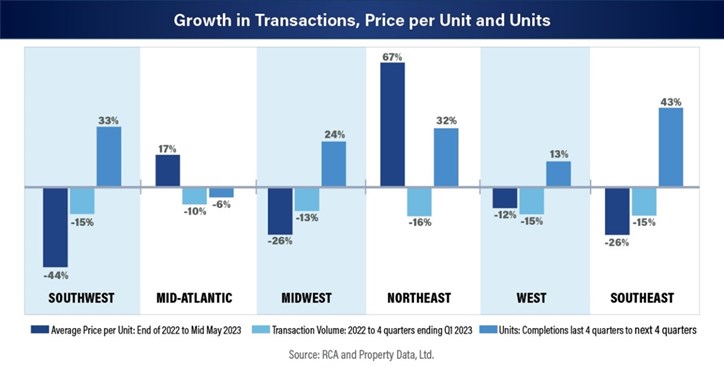

A DEEPER LOOK – REGIONAL APARTMENT MARKETS

Approximately 1 million apartment units were underway in early 2023. Once completed, it is unclear how much they will affect rents and property valuations. An examination of recent transaction and price per unit performance in the six major regions may reveal some impacts.

In the Northeast, although the transaction volume drop was on par with other regions, the average price per unit rose. In 2023, the number of new units is expected to jump by almost 30 percent, although prices may not move much. According to the National Association of REALTORS®, New York City and Boston were #1 and #8 in net absorption* in Q1 2023.

The Mid-Atlantic market shrunk less than average and price per unit improved, reflecting the strength of both the Washington D.C. and Philadelphia metropolitan areas. According to MSCI, the District of Columbia had two of the top five largest single apartment transactions in Q1 2023. With a six percent fall in unit completions in the next year, this region may continue to see price per unit increases.

The Southeast is the market where new units could have the most impact. Transactions and price per unit were down, particularly in Orlando, Florida. MSCI shows that all major metro areas except Nashville, Tennessee will be adding more units than they did last year.

WHAT’S NEXT?

To see how the quarter unfolds, stay tuned for next month’s Economic Update Q2 2023.

*Copyright ©2023 “Commercial Market Insights Report – April 2023.” NATIONAL ASSOCIATION OF REALTORS®. All rights reserved. Reprinted with permission. June 2023, https://www.nar.realtor/commercial-market-insights/april-2023-commercial-market-insights.