MARKET OVERVIEW

There were signs that the plunge in prices and transaction volumes may have bottomed out. RCA’s Commercial Property Price Index (CCPI) declines continued to moderate in October. Although activity was down 53 percent in Q3 compared to last year, transactions hovered around $90 billion for each quarter in 2023, according to MSCI. Selective deal making was made possible by solid economic underpinnings. Retail vacancies were only 4.2 percent in Q3, thanks to a shortage of available space and remarkable consumer spending. Record industrial space deliveries pushed the vacancy rate higher last quarter, but it was below pre-pandemic averages and asking rent growth remained robust. The enduring travel boom further boosted hotel occupancy rates, while downward rent and price pressures on the Multifamily sector tempered as unfavorable home buying conditions supported apartment demand.*

Investors were very focused on interest rates. Concerns that rates will stay higher for longer not only hurt valuations and borrowing costs, but also banks’ balance sheets and, thus, their amenability for lending (or loan modifications). Delinquency rates ticked up 0.4 percent in Q3, but most properties are too early in the foreclosure process to lead to many distress deals. Office properties accounted for most of the increase and this sector’s fundamentals remain uncertain. In November, the bankruptcy of office-sharing company WeWork increased the market’s apprehension – the national office vacancy rate was already 21 percent in Q3, per JLL. The post-Labor Day return to office was not the surge landlords had hoped, with hybrid being the new normal. Attendance rates are expected to be 55 percent by year end, but still significantly below pre-pandemic levels.

A DEEPER LOOK – OFFICE DELIVERIES BY REGION

Lenders expect to tighten credit availability for the end of the year, especially for construction and land development loans. The silver lining is that this could put a floor under property valuations. JLL’s U.S. Office Outlook for Q3 2023 noted that the office development pipeline has declined over 33 percent in the last five quarters. The report surmised that “…not only will rental rates in new and trophy offices begin to experience upward pressure, but landlords of non-trophy properties may begin to see spillover demand as availability declines.”

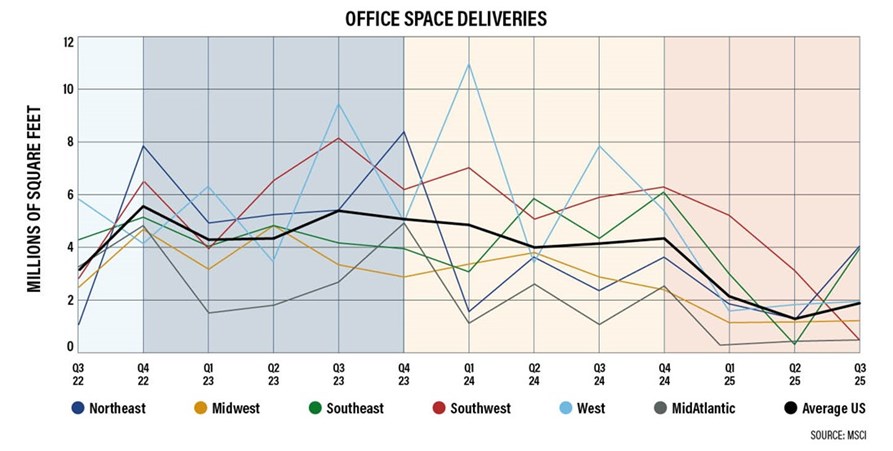

The graph below looks at the expected deliveries of office space by region. At the end of 2022, the regions were bunched together and mostly on the upswing. But they have diverged in 2023, and a downturn over the course of 2024 and into 2025 is projected.

In the Mid-Atlantic, DC’s market contraction will be somewhat mitigated by deliveries in the Philly area. A downward movement in Chicago’s office deliveries dominates the Midwest’s trajectory. The Northeast’s precipitous drop-off in 2024 demonstrates metro New York’s retrenchment, which is slightly countered by Boston’s building (likely due to a surge of lab space). The West’s seesaw inventory reflects twin movements in both San Francisco and Seattle technology centers. The Southeast’s comparatively gentle path is driven by fluctuations in Nashville and Raleigh/Durham, while Atlanta is expected to be a consistent contributor over the next four quarters.

WHAT’S NEXT?

Stay tuned for next month’s Economic Update Q4 2023 to see how the year ends.

*Copyright ©2023 “Commercial Market Insights Report – October 2023.” NATIONAL ASSOCIATION OF REALTORS®. All rights reserved. Reprinted with permission. November 2023, https://www.nar.realtor/commercial-real-estate-market-insights/october-2023-commercial-real-estate-market-insights.